When you fill a prescription, you might see a charge on your card that doesn’t match what the pharmacy told you. You thought your insurance covered it - so why did you pay $75 for a $20 drug? That’s cost sharing in action. It’s not a trick. It’s how most health plans in the U.S. work. You’re not paying the full price, but you’re not getting it free either. Your plan splits the cost with you - and that split comes in three forms: deductibles, copays, and coinsurance. If you’ve ever been confused by these terms, you’re not alone. Even people who’ve had insurance for years mix them up. Let’s break it down, plain and simple.

What’s a Deductible? (And Why It Matters for Medications)

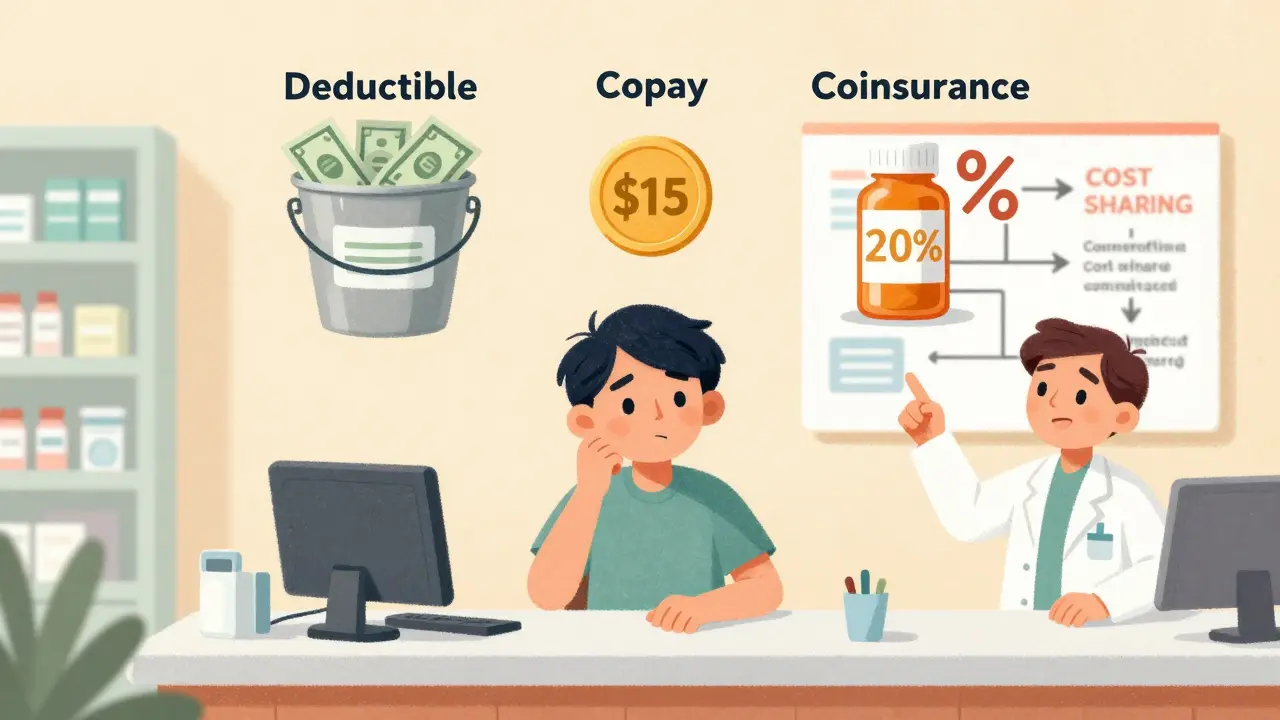

Your deductible is the amount you pay out of pocket each year before your insurance starts helping with most costs. Think of it like a bucket. Every time you pay for a doctor visit, lab test, or prescription, that money goes into the bucket. Once the bucket is full - meaning you’ve spent your deductible amount - your insurance kicks in to cover part of the rest.

For medications, this means if your plan has a $1,500 deductible, you pay 100% of your drug costs until you’ve spent that much. A $120 insulin refill? You pay it all. A $300 specialty medication? Still you. No help from insurance yet. Once you hit $1,500 in total out-of-pocket spending on covered services (including meds), then coinsurance or copays start applying.

High-deductible plans are common. In 2023, the average deductible for individual plans was around $1,945. Bronze plans often have deductibles over $7,000. These plans usually have lower monthly premiums, but you pay more upfront when you need care. If you’re healthy and rarely take meds, this might make sense. If you’re on chronic meds - say, for diabetes or high blood pressure - you’ll likely hit your deductible fast and end up paying more overall.

Copays: Fixed Fees at the Pharmacy Counter

A copay is a flat fee you pay each time you get a service. For prescriptions, it’s usually $10, $20, or $40 - no matter how much the drug actually costs. You don’t need to meet your deductible first for copays to apply. Many plans have copays for medications even before you hit your deductible.

Here’s how it works: Your plan might have a $15 copay for generic drugs and $45 for brand-name ones. You walk into the pharmacy, hand over your card, and pay $15. The insurance company pays the rest. Even if your deductible hasn’t been met, you still pay only $15. That’s because copays are designed to make routine care predictable.

But here’s the catch: Not all plans use copays for meds. Some, especially high-deductible plans, make you pay full price until you hit your deductible. Then, and only then, do copays or coinsurance kick in. Always check your plan’s Summary of Benefits. It’ll say exactly when copays apply.

Preventive services - like annual check-ups or certain vaccines - are often covered at $0 copay, even before you meet your deductible. That’s thanks to the Affordable Care Act. But that rule doesn’t extend to most medications. Only a few, like certain birth control pills or diabetes supplies, are guaranteed free.

Coinsurance: The Percentage You Pay After the Deductible

Coinsurance is where things get tricky. It’s not a fixed amount. It’s a percentage. After you meet your deductible, you pay a portion of each drug’s cost - and your insurance pays the rest.

Let’s say your coinsurance is 20%. You need a $100 prescription. You’ve already paid your $1,500 deductible. Now, you pay $20. Your insurance pays $80. Simple, right? But here’s the twist: That $100 isn’t necessarily what the drug costs. Insurance companies negotiate prices with pharmacies. That $100 is the “allowed amount.” The pharmacy might charge $150, but your plan only agrees to pay up to $100. You pay 20% of $100 - $20. The extra $50? You don’t pay it. That’s a good thing.

Coinsurance often applies to specialty drugs - the expensive ones for conditions like rheumatoid arthritis, MS, or cancer. Those can cost $1,000 a month. With 30% coinsurance, you’d pay $300. That’s a big hit. Some plans have tiered coinsurance: 10% for generics, 25% for brand-name, 50% for specialty. Always ask your insurer: “What’s my coinsurance rate for this drug?”

Out-of-Pocket Maximum: The Safety Net

Here’s the good news: You won’t pay forever. Every plan has an out-of-pocket maximum. In 2023, that cap was $9,100 for an individual and $18,200 for a family. This includes all your deductibles, copays, and coinsurance payments - but not your monthly premiums.

Once you hit that limit, your insurance pays 100% of covered services for the rest of the year. That means if you’re on a $2,000-a-month specialty drug, and you’ve already paid $9,100 in out-of-pocket costs, the next $2,000? Your insurance covers it all.

Many people think their out-of-pocket maximum includes premiums. It doesn’t. Premiums are what you pay every month just to have coverage. Out-of-pocket costs are what you pay when you actually use care. Confusing the two leads to nasty surprises. A 2022 survey found 42% of people mistakenly thought premiums counted toward their out-of-pocket max. Don’t be one of them.

How These Three Work Together

Here’s a real-life example:

- You have a $2,000 deductible, 20% coinsurance, and a $9,100 out-of-pocket max.

- January: You fill a $300 prescription. You pay $300 (deductible not met).

- February: Another $400 med. You pay $400. Total paid: $700.

- March: A $1,000 specialty drug. You pay $1,000. Total: $1,700.

- April: Another $1,000 drug. You pay $300 this time - because you’ve now met your $2,000 deductible. Now, coinsurance starts.

- May: You get a $500 drug. You pay 20% = $100. Insurance pays $400.

- By November, you’ve paid $9,100 total. December: You need another $1,200 drug. You pay $0. Insurance covers it.

That’s how it flows. Deductible first. Then coinsurance. Always capped by your out-of-pocket maximum.

What You Should Do Right Now

You don’t need to be an expert. But you do need to know three things about your plan:

- What’s your deductible? Check your plan documents. If you’re on meds, know if you’ll hit it fast.

- What’s your coinsurance rate for your drugs? Call your insurer. Ask: “For [drug name], what’s my cost after I meet my deductible?”

- Is your pharmacy in-network? Out-of-network pharmacies can charge way more. Your coinsurance might jump from 20% to 50%.

Use your insurer’s online cost estimator. Most have one. Type in your drug name. It’ll show you estimated costs at different pharmacies. You might save $50 or $200 just by switching.

And always ask: “Is this covered before my deductible?” Some plans cover certain meds - like diabetes or blood pressure drugs - even before you meet your deductible. You might not know unless you ask.

What’s Changed in 2025

The Inflation Reduction Act capped insulin at $35 per month for Medicare users - and that’s now standard. Many private insurers have followed suit. Some now cap other chronic disease meds too.

Also, the No Surprises Act protects you from surprise bills if you get care at an in-network hospital but see an out-of-network doctor. That applies to meds too. If your pharmacy is in-network, you shouldn’t get a surprise charge for your prescription.

By 2025, more plans will use “value-based design.” That means lower cost sharing for high-value drugs - like those that prevent hospital visits - and higher cost sharing for low-value ones. It’s not perfect, but it’s a step toward smarter spending.

Final Thought: Know Your Numbers

Health insurance isn’t about what’s covered. It’s about what you pay. A plan with a $100 monthly premium and a $7,000 deductible might look cheap. But if you take two expensive meds a month? You’ll pay more than someone with a $500 premium and a $500 deductible.

Don’t choose a plan based on premium alone. Look at the whole picture: deductible, coinsurance, out-of-pocket max, and how your meds fit into it. A $20 copay on a $500 drug sounds great - until you realize you’re paying $20 every month for a year. That’s $240. That’s more than the cash price at some pharmacies.

Know your numbers. Ask questions. Use tools. You’re not just paying for medicine. You’re paying for a system. And you deserve to understand it.

Do copays count toward my deductible?

It depends on your plan. Some plans count copays toward your deductible. Others don’t. Most high-deductible plans require you to pay full price until the deductible is met - even if you have copays. Always check your plan’s Summary of Benefits. It’ll say exactly how copays are treated.

Can I pay less for my medication if I don’t use insurance?

Yes - sometimes. Many generic drugs cost less out-of-pocket than your insurance copay. For example, a 30-day supply of lisinopril might be $4 at Walmart or Costco, but your copay is $15. Always ask the pharmacy for the cash price before using insurance. You can also use GoodRx or SingleCare coupons to compare prices.

What if I can’t afford my coinsurance on a specialty drug?

Many drug manufacturers offer patient assistance programs. These can reduce or eliminate your coinsurance. Ask your pharmacist or doctor - they often have access to these programs. Nonprofits like the Patient Advocate Foundation and NeedyMeds also help people with high drug costs. Don’t skip meds because you think you can’t pay. Help exists.

Do preventive medications count toward my deductible?

Most preventive services - like vaccines or screenings - are covered at $0 and don’t count toward your deductible. But most medications, even if they prevent disease (like statins or blood pressure pills), do count toward your deductible unless your plan specifically says otherwise. Check your plan’s rules.

Why does my coinsurance change depending on the pharmacy?

Because pharmacies negotiate different prices with insurers. Your plan has a negotiated rate with each pharmacy. If you go to an out-of-network pharmacy, your coinsurance percentage might go up - say from 20% to 40% - and the allowed amount might be higher. Always use in-network pharmacies. It saves you money.

Next Steps: What to Do Today

- Log into your insurance portal. Find your Summary of Benefits. Look for the section on cost sharing.

- Write down your deductible, coinsurance rate for your top 3 meds, and your out-of-pocket max.

- Call your pharmacy. Ask: “What’s the cash price for [drug]?” Compare it to your copay.

- Set a reminder: Every January, review your plan. Costs change yearly.

Understanding cost sharing isn’t about becoming a financial expert. It’s about not getting blindsided. You’re paying for care. Make sure you know exactly how much - and why.

matthew runcie

March 22, 2026 AT 04:34Just saved me a headache next time I refill my blood pressure med.

Nicole James

March 23, 2026 AT 03:28Nishan Basnet

March 23, 2026 AT 17:30Timothy Olcott

March 25, 2026 AT 05:36Jackie Tucker

March 26, 2026 AT 09:04Thomas Jensen

March 26, 2026 AT 10:54shannon kozee

March 26, 2026 AT 20:32trudale hampton

March 28, 2026 AT 17:51Shaun Wakashige

March 29, 2026 AT 08:46Paul Cuccurullo

March 30, 2026 AT 01:35Johny Prayogi

March 31, 2026 AT 11:04Allison Priole

April 1, 2026 AT 19:58Sandy Wells

April 1, 2026 AT 22:15Bryan Woody

April 3, 2026 AT 04:36